Listen to this blog

In recent years, as mortgage interest rates have remained consistently high, it has impacted the overall mortgage business, including mortgage lenders who are now looking to tap into other verticals to fill the void. Non-QM loans serve as a brilliant alternative and an add-on to existing verticals, mostly due to the rise of gig economy.

Since the pandemic, there has been a dramatic shift in workplace dynamics. Young professionals are prioritizing flexible work arrangements and considering self-employment at unprecedented rates. Now, as demographic trends shift away from traditional employment towards entrepreneurial self-employment and the gig economy, mortgage lenders should anticipate a greater number of self-employed applicants seeking mortgage loans, with millennial and ‘Generation Z’ applicants becoming primary consumers in the housing market. Thus, the mix of borrowers is the most important determinant in non-QM performance, because non-QM borrowers, such as self-employed individuals and real estate investors, are less rate-sensitive.

However, utilizing the traditional process of manual loan execution and underwriting a self-employed mortgage loan application can take significantly longer to analyze than a traditional one. Because of this added complexity, many mortgage lenders shun or undervalue this type of non-traditional applicant, despite their underlying potential.

In this blog, we will delve deeper into the various nuances of the non-QM market, learn about the different terminologies, and explore how they can add value to the mortgage lender's portfolio.

Decoding non-QM

First, let us try to understand the distinctions between Qualified Mortgage (QM) and Non- Qualified Mortgage (Non-QM). The term ’qualified mortgage’ refers to a lender's compliance with various CFPB agency requirements, including the Ability-To-Repay (ATR) Rule

Non-QMs, on the other hand, are not guaranteed by government organizations such as Freddie Mac or Fannie Mae, nor are they insured by the U.S. Department of Agriculture, the Department of Veterans Affairs (VA), or the Federal Housing Administration (FHA). Non-QMs fail to meet at least one of the requirements.

What are the typical characteristics of non-QM loans?

The most prevalent loan features that do not comply with these rules are:

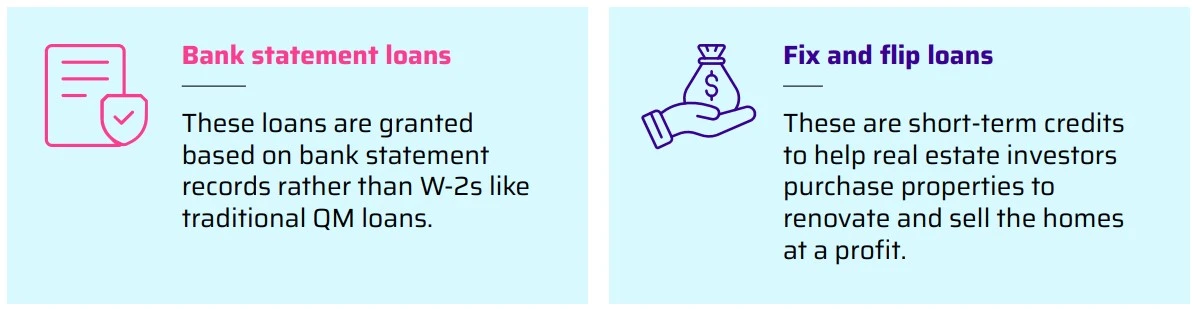

Following are the different types of non-QM products being originated these days:

Debt Service Coverage Ratio (DSCR) loans: These loans are underwritten based on the cash flow generated from investment properties rather than a borrower’s income.

Challenges in non-QM lending: Navigating growth and risk

Under U.S. law, mortgage applicants must meet specific qualifications and adhere to guidelines issued by the FHA, VA, or USDA. The necessary conditions include the following:

Furthermore, the mortgage applicant's loan request must not exceed the agency limits set by the USDA, VA, or FHA. Borrowers that do not meet the aforementioned conditions may be able to acquire non-QM loans, allowing for more flexible underwriting requirements.

However, for these kinds of non-qualified mortgages, it's also crucial for lenders and borrowers to follow federal laws such as the Equal Credit Opportunity Act and the Fair Housing Act.

Non-QM loans, by their very nature, are typically more difficult to handle and traditionally entail significantly more manual work than agency loans

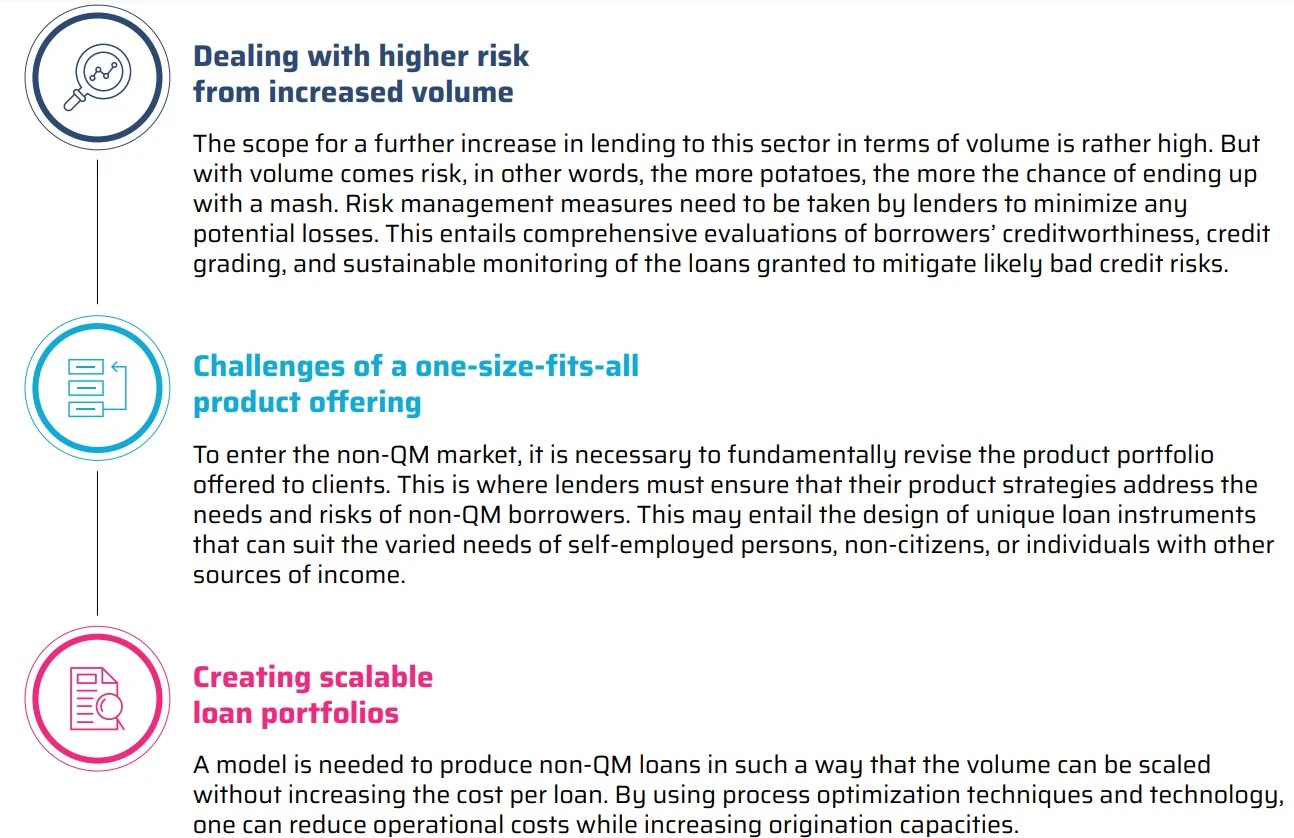

Thus, while the non-qualified mortgage or (non-QM) market has the potential for significant expansion, it also presents particular challenges that require to be addressed in a different way to increase growth in this line of business.

Let's analyze these challenges and find out what they are all about.

Therefore, non-QM lending presents numerous opportunities for attractive growth rates. Yet, it also comprises certain risks that must be skillfully controlled. At the same time, it is essential to determine product activities and enhance operational performance.

Mitigating the risk and enhancing the growth of non-qualified mortgages through efficient business processes and technological solutions

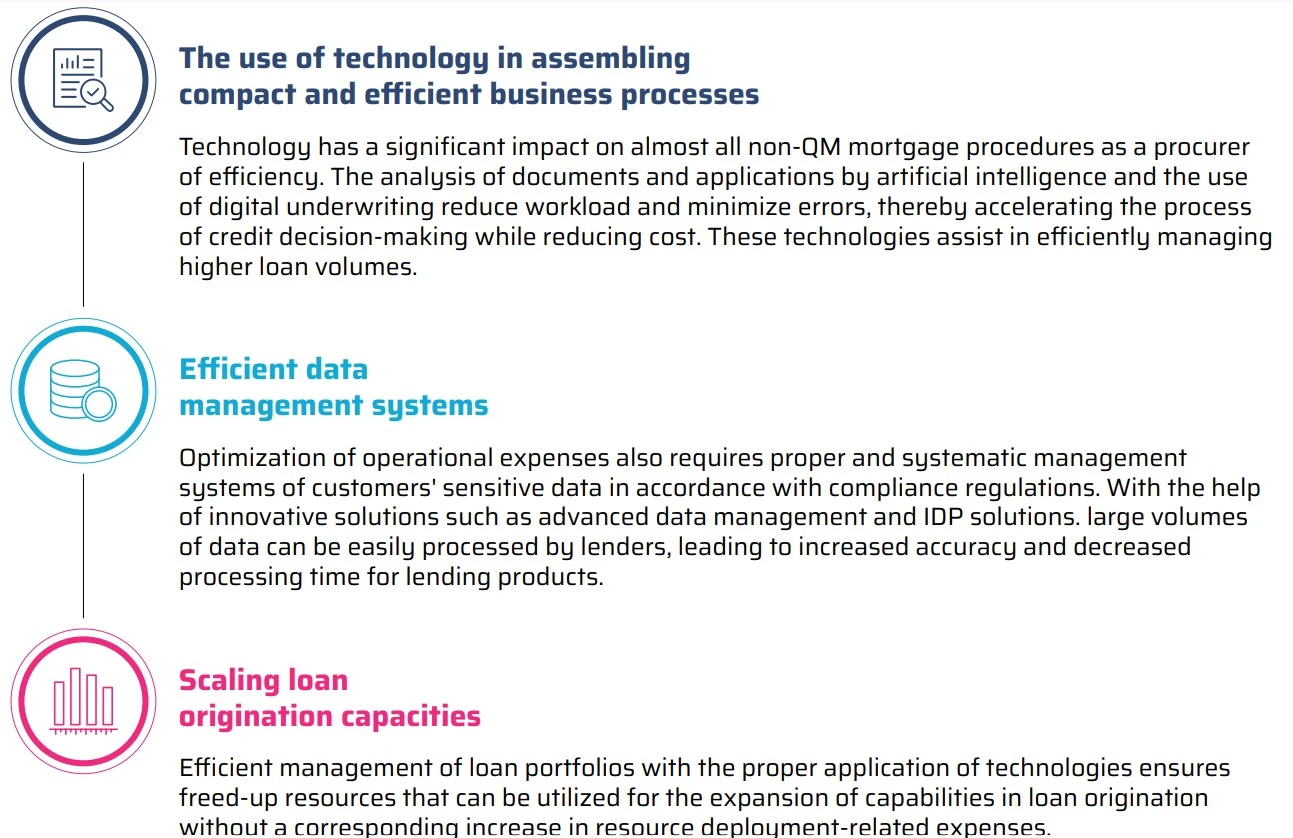

Lenders seeking to maximize returns and minimize costs in the non-QM market must effectively manage these loans through a combination of process optimization and technology solutions. This approach will help strike a balance between growth and risk, positioning them for success in non-qualified mortgage lending. Thus, the key to maintaining the profitability of the enterprise lies largely in minimizing costs for processing non-QM loans.

Here are a few such techniques summarized below:

While non-QM lending offers promising growth prospects, success hinges on efficiently managing loan volumes and costs in managing non-QM loans without escalating costs per loan. Leveraging technology for streamlined processes such as automated document verification, digital underwriting tools, and efficient data management systems, can help minimize operational expenses while scaling loan origination capacities. Striking a balance between these factors can enable growth while cutting down on risk

Conclusion

With a significant rise in demand for non-QM loans when other loans are experiencing volume drop-offs, selecting the right mortgage partner to assist in audit and risk management processes for non-QM lenders will offset some of the negative aspects of non-QM loans, making the lenders more competitive.

In this regard, lenders of non-QM services look for unique solutions to handle the complexities of the origination and underwriting of non-QM loans.

With a deep understanding of the mortgage industry from several decades of operation, Visionet is capable of offering tailor-made solutions for the non-QM market.

From calculating income for the self-employed borrower, which is often far more complex than conventional mortgage loans, to handling document-heavy non-QM loan files, to providing automation solutions for the streamlined processing of documents and data that can capture risk before loans are sold during secondary transactions, Visionet has what it takes to make non-QM businesses profitable and risk-resilient.

Partner with Visionet to simplify non-QM loan processing, reduce risk, and boost profitability. Contact us today to learn how our tailored solutions can give you a competitive edge.